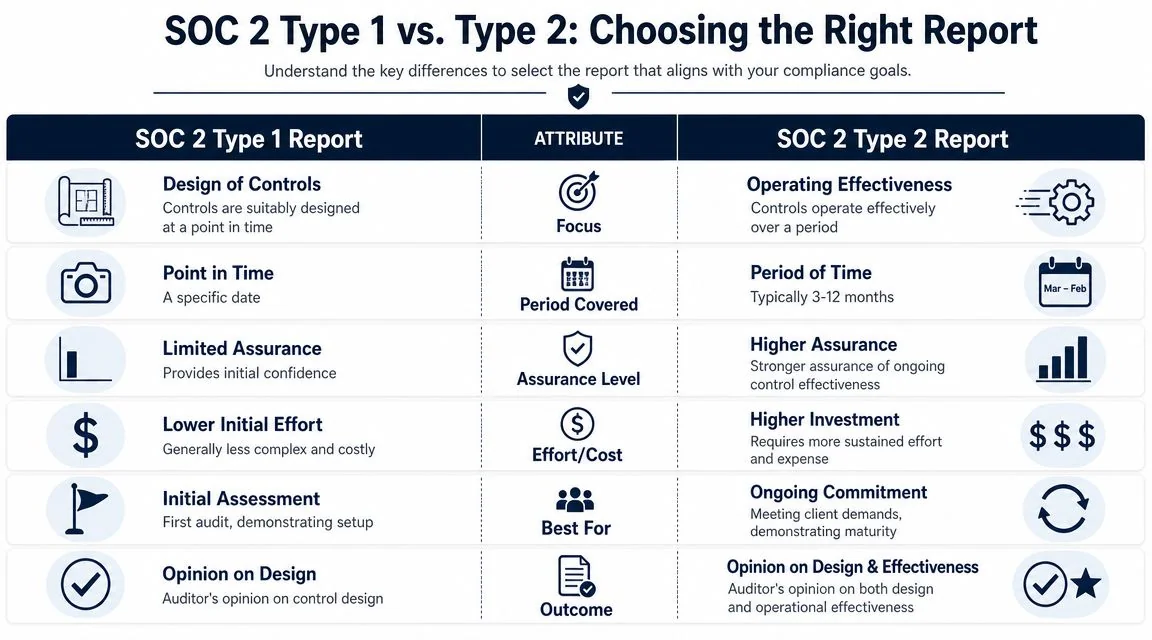

For many small software and service companies, SOC 2 is technically voluntary but commercially mandatory. A SOC 2 audit is an attestation performed by a licensed CPA firm against the AICPA Trust Services Criteria, and for a first report the practical choice is between Type 1, which evaluates whether controls are designed correctly at a single point in time, and Type 2, which evaluates whether those controls operate effectively over a period that is typically 3 to 12 months according to The Core Solution’s SOC 2 small business overview. That distinction matters because most enterprise buyers prefer Type 2 reports, and the work required to get there affects budget, staffing, sales timing, and auditor choice.

For a founder, the key mistake is treating a soc 2 audit for small business as a narrow security task. It’s a business decision with direct impact on deal velocity, internal workload, and how much process discipline your team can sustain while the company keeps shipping product.

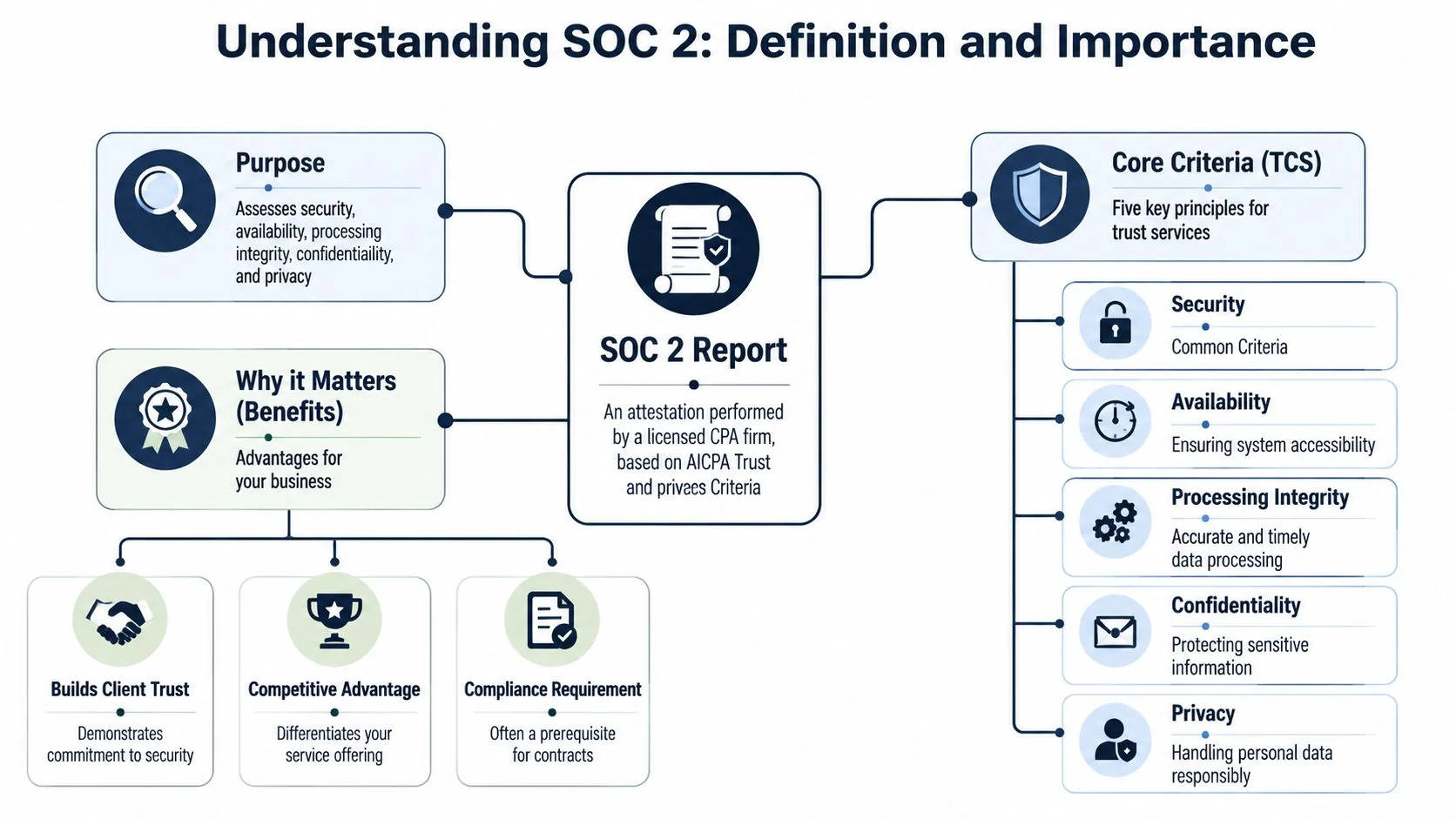

What Is a SOC 2 Audit and Why Does It Matter

A single enterprise prospect can stall a six-figure deal if your team cannot answer basic security diligence with evidence. That is why a SOC 2 audit shows up earlier than many founders expect.

A SOC 2 audit is an independent attestation performed by a licensed CPA firm for service organizations that store or process customer data. It is built on the AICPA Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy. Security is required in every SOC 2 engagement. The other criteria depend on what you sell, how your product works, and which customer commitments you make.

SOC 2 is different from SOC 1 in a way that has direct commercial impact. SOC 1 focuses on controls relevant to financial reporting. SOC 2 focuses on security, availability, and related system controls. If you run a SaaS company, managed service provider, or data-handling service business, buyers usually care about SOC 2 because it helps them assess operational risk, not accounting risk.

Why small businesses get asked for it

Small companies rarely pursue SOC 2 for prestige. They do it because revenue pressure forces the decision. A prospect’s procurement team asks for a report. A security review blocks legal. A larger customer agrees to move forward only if the company can show a defined control environment and a credible audit timeline.

That changes the conversation. SOC 2 stops being a technical side project and becomes a business filter for who you can sell to, how long deals take to close, and how much founder time gets pulled into diligence.

For a straightforward baseline, see this overview of what SOC 2 compliance means. Teams comparing implementation approaches can also review tools and workflow examples such as Formbricks SOC 2 compliance.

Practical rule: If a prospect is asking for access review records, incident response procedures, logging practices, and vendor management details, your company is already being evaluated like a SOC 2 organization.

What matters operationally

Founders often underestimate where the cost sits. Audit fieldwork is visible, but the expensive part is the operating model behind it. If your team has to scramble for screenshots, rewrite policies during sales cycles, or manually chase evidence across Slack and Jira, the audit cost is only part of the bill. The larger cost is slower delivery, distracted engineers, and delayed revenue.

For a small business, four decisions shape whether SOC 2 becomes an asset or a drain:

-

What systems are in scope

If scope is too broad, you add avoidable audit hours and internal work. If scope is too narrow, customers may reject the report because it does not cover the product or environment they use. -

Who owns each control Access reviews, change approvals, incident handling, and vendor checks need named owners. Without ownership, controls fail unnoticed until the auditor asks for evidence.

-

What evidence exists today

Auditors test artifacts, not intent. If evidence collection is manual, expect more time from engineering, IT, and leadership during the audit cycle. -

Whether the team can maintain the program

A report helps only if the controls keep running after issuance. Small companies get into trouble when they build a one-time audit project instead of a repeatable operating process.

A soc 2 audit for small business matters because it affects sales timing, staffing load, and vendor spend at the same time. Handled well, it shortens security reviews and gives buyers confidence. Handled poorly, it turns into a long, expensive exercise that still fails to remove friction from the sales process.

The Critical Decision Type 1 vs Type 2 Reports

The first serious decision isn’t which tool to buy. It’s whether you need a Type 1 report now, a Type 2 report as the ultimate goal, or both in sequence.

A Type 1 report evaluates whether your controls are suitably designed at a single point in time. A Type 2 report evaluates both design and operating effectiveness over an observation period. For small businesses, the standard path is often Type 1 first, then immediate evidence collection for Type 2, which can require 3 to 12 months of observation plus another 4 to 6 weeks for the Type 2 audit, according to Sprinto’s small-business SOC 2 guidance.

When Type 1 makes sense

Type 1 is usually the right move when speed matters more than depth. A founder may need something credible for an active pipeline, investor diligence, or a customer that will accept a point-in-time report as an interim step.

Type 1 also gives a first-time team a way to validate scope and control design before living under observation for months. That can be useful if your policies are drafted, your control owners are identified, and your core systems are reasonably stable, but your evidence discipline is still immature.

When Type 2 is the real requirement

Most mature buyers prefer Type 2 because it shows sustained performance, not just a clean setup on one date. If your target customers are large enterprises, regulated buyers, or security-heavy procurement teams, you should assume Type 2 is the destination even if Type 1 gets you through the first door.

The hidden issue is not the audit week. It’s the operating period. During those months, your team has to keep controls working while onboarding employees, shipping code, replacing vendors, and changing infrastructure.

The hard part isn’t writing the policy. The hard part is proving the process still worked after the company changed around it.

A simple decision filter

Use this lens:

| Question | Lean toward Type 1 | Lean toward Type 2 |

|---|---|---|

| Current sales need | You need a report quickly for near-term deals | Buyers already expect ongoing assurance |

| Control maturity | Controls are designed but not yet consistently evidenced | Controls already run on a repeatable cadence |

| Team capacity | Limited compliance bandwidth right now | You can sustain monthly and quarterly routines |

| Customer expectations | Prospects will accept an interim report | Procurement teams ask for stronger evidence |

A soc 2 audit for small business goes wrong when founders treat Type 1 as the finish line. In many cases, it’s better understood as a staging point. If you choose it, choose it with a Type 2 operating plan already in place.

Estimating Your SOC 2 Costs and Timelines

Small teams usually underestimate SOC 2 in two ways. They focus on the auditor fee and ignore internal time, and they assume the calendar follows the same pace as the sales pipeline.

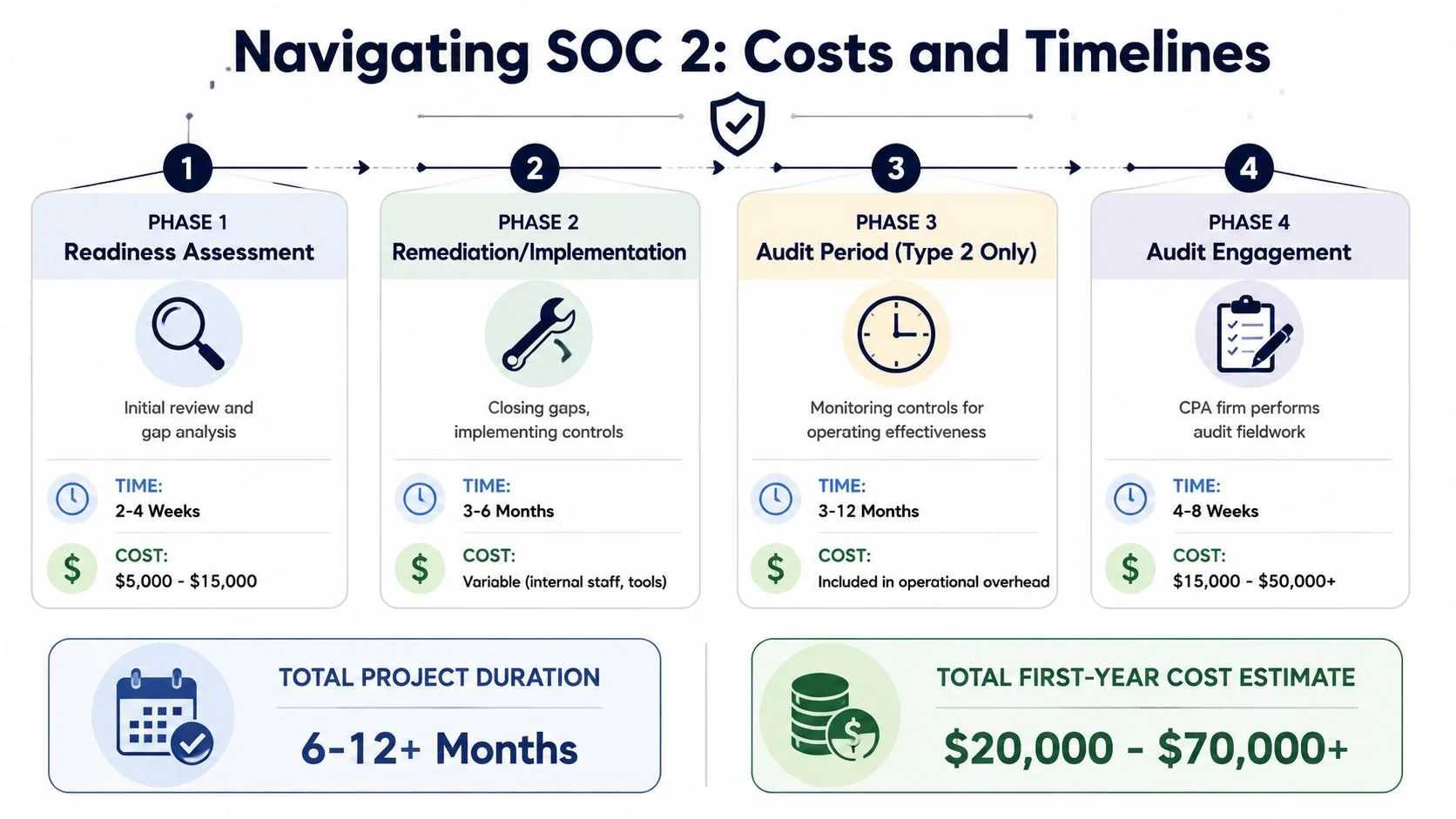

For small businesses, one estimate puts Type 1 audit cost at roughly $12,000 to $20,000 and Type 2 at roughly $15,000 to $50,000, with the process often consuming 50% or more of a senior person’s time for three to six months on Type 1 and requiring ongoing attention during a 6- to 12-month Type 2 period, according to SkyTerra’s SOC 2 cost breakdown.

Where the real cost sits

The auditor invoice is visible. The internal drag is what hurts.

A founder, CTO, head of engineering, or ops lead usually becomes the default SOC 2 owner. That person spends time coordinating policy work, assigning control ownership, cleaning up access, organizing evidence, answering auditors, and chasing exceptions. If that owner also runs product delivery or customer operations, SOC 2 competes directly with revenue-generating work.

Budget categories to plan for

You need a practical budget, not just an audit quote.

-

Audit fee

This is the CPA firm cost for the engagement itself. -

Readiness support

Some teams use consultants, internal security staff, or platform-based guidance to prepare controls before fieldwork. -

Tooling and evidence collection

Compliance automation can reduce manual collection, but it doesn’t replace control ownership or auditor review. -

Internal labor

This is usually the largest unplanned cost because it cuts across engineering, IT, HR, and leadership.

If you’re trying to map the calendar realistically, this guide on how long a SOC 2 audit takes is a useful planning reference.

What affects your timeline most

The fastest projects are tightly scoped and run by teams that already have discipline around access, change approval, logging, and vendor review. The slowest projects usually have one of these traits:

- Scope bloat that pulls in systems not needed for the initial report

- Weak evidence habits where controls happen informally but nothing is documented

- Undefined ownership so tasks sit idle between meetings

- Business churn such as major tooling changes during the audit window

A realistic SOC 2 plan starts with staffing, not optimism. If no one has protected time to run the program, the timeline is already slipping.

For a small business, the business case isn’t just whether you can afford the audit. It’s whether you can afford to start late, scope poorly, and burn months of senior attention cleaning up preventable issues.

The Step-by-Step SOC 2 Audit Workflow

Most first audits break down before fieldwork starts. The usual cause isn’t that the auditor is unreasonable. It’s that the company started the project without a narrow scope, named owners, or a repeatable evidence process.

For small businesses, a common failure mode is weak control design and undefined control ownership during readiness, and firms that skip readiness often increase duration and cost because they can’t produce evidence that controls operated repeatedly over time, as noted in Linford & Co.’s readiness guidance for startups.

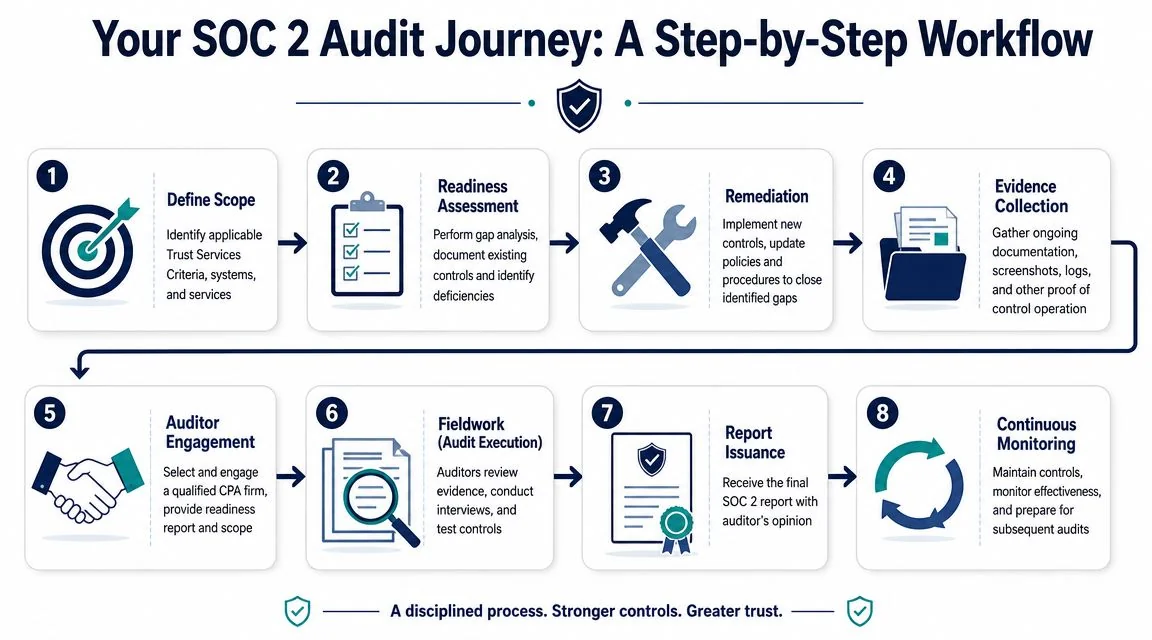

Step 1 and Step 2 define scope and test readiness

Start with scope. Limit it to the systems and services that store, process, or transmit customer data. Founders often make an expensive mistake related to scope by pulling in every internal tool and every side system “just to be safe.”

Then run a readiness assessment. That means checking whether required controls exist, whether they match the selected Trust Services Criteria, and whether someone can prove they operate.

A useful readiness review usually covers:

- Access management for user provisioning, removals, privileged access, and periodic reviews

- Change management for code, infrastructure, and production changes

- Logging and monitoring so activity can be reviewed and investigated

- Vulnerability remediation so findings are tracked and resolved

- Vendor oversight for third parties that affect customer data or service delivery

Step 3 and Step 4 remediate and collect evidence

After gaps are identified, fix the process before you polish the document. If your team says it reviews access quarterly, make sure that review takes place, leaves a record, and has an owner.

This is also the point where evidence discipline needs to become routine. Screenshots, tickets, logs, approvals, review notes, training acknowledgments, and vendor records all matter. The issue isn’t volume. It’s consistency and traceability.

Here’s a practical rhythm that works better than a last-minute scramble:

- Set a control calendar for monthly, quarterly, and annual activities.

- Store evidence in one place with clear naming and dates.

- Review completeness every month so missing artifacts are fixed early.

- Escalate broken controls quickly instead of hoping the gap won’t be tested.

To see the process in a different format, this short walkthrough is useful:

Step 5 through Step 8 work with the auditor and maintain the program

Once the environment is ready, engage the CPA firm, confirm scope, align on requests, and prepare stakeholders for interviews. During fieldwork, auditors review evidence, ask follow-up questions, and test whether the controls described match operational reality.

After issuance, the report needs to be usable. Sales should know how to position it. Security or legal should know how to share it under NDA. Leadership should review any exceptions and fix the underlying process, not just the paperwork.

A soc 2 audit for small business becomes manageable when the team treats it like an operating system. Scope narrowly. Assign owners. Collect evidence as you go. Keep the process alive after the report lands.

How to Choose the Right SOC 2 Auditor

Many small businesses make the most expensive avoidable decision. They spend weeks preparing controls, then pick an auditor based on brand recognition alone or the lowest quote in the inbox.

One market guide notes that SOC 2 costs can range from $20,000 to over $150,000 and that buyers often lack a structured way to compare firms on speed, evidence burden, and report quality, according to A-LIGN’s SOC 2 overview. That range should tell you one thing immediately: auditor selection isn’t administrative. It’s strategic.

The three firm types

| Firm Type | Typical Cost (Type 2) | Best For | Pros | Cons |

|---|---|---|---|---|

| Big Four | Higher end of market | Large enterprises, complex environments, buyers that care about firm brand | Strong name recognition, broad service lines, familiarity with complex structures | Higher cost, less flexibility, often heavier process burden for smaller teams |

| Mid-tier firms | Mid-market range | Growing companies that want balance between rigor and budget | More accessible than Big Four, usually solid process maturity, reasonable brand acceptance | Quality varies by office and team, experience may differ by industry |

| Specialist firms | Often more budget-sensitive for startups, but varies | First-time SOC 2, SaaS startups, teams that need guidance and responsiveness | Typically faster, more hands-on, often better fit for narrow scopes | Less brand weight with some procurement teams, quality can vary widely |

What actually matters in the selection process

Most founders ask, “Can you do SOC 2?” That question is too broad to be useful. Every candidate firm will say yes. The better question is whether they fit your company’s pace, scope, and internal maturity.

Look at these factors instead:

-

Responsiveness

If a firm takes days to answer basic scoping questions before the contract, expect delays during the audit. -

Evidence burden

Some auditors are pragmatic. Others create work that swamps a small team. Ask what artifacts they normally request for access reviews, changes, incidents, and vendor controls. -

Industry fit

A firm that understands SaaS, MSP, fintech, or health data workflows will scope faster and ask sharper questions. -

Project cadence

You need to know who runs the engagement, how request lists are managed, and how exceptions are handled. -

Report usability

A technically valid report that creates confusion during customer diligence still causes commercial pain.

Ask the auditor how they handle a startup that changes tools mid-observation period. The answer will tell you whether they understand real operating environments or only ideal ones.

Questions worth asking before you sign

Use direct questions, not generic vendor due diligence.

- How do you scope first-time small-business audits to avoid unnecessary systems?

- What does your evidence request list typically look like for a SaaS company?

- Who will manage the engagement day to day?

- How do you handle control exceptions discovered during fieldwork?

- What slows projects down most often from your side and from the client side?

- How much support do you provide before fieldwork starts?

- How do you approach fast-changing environments with new hires, tooling changes, or product releases?

If you want a structured way to compare firms on pricing, scope fit, and timelines, one option is SOC2Auditors, which catalogs SOC 2 audit firms and comparison data to help buyers narrow the field before outreach. Used correctly, a comparison platform saves time. It doesn’t replace judgment. You still need to assess whether the firm’s process matches your internal capacity.

The right auditor for a small business is rarely the most famous one. It’s the one whose process your team can survive without derailing product, sales, and operations.

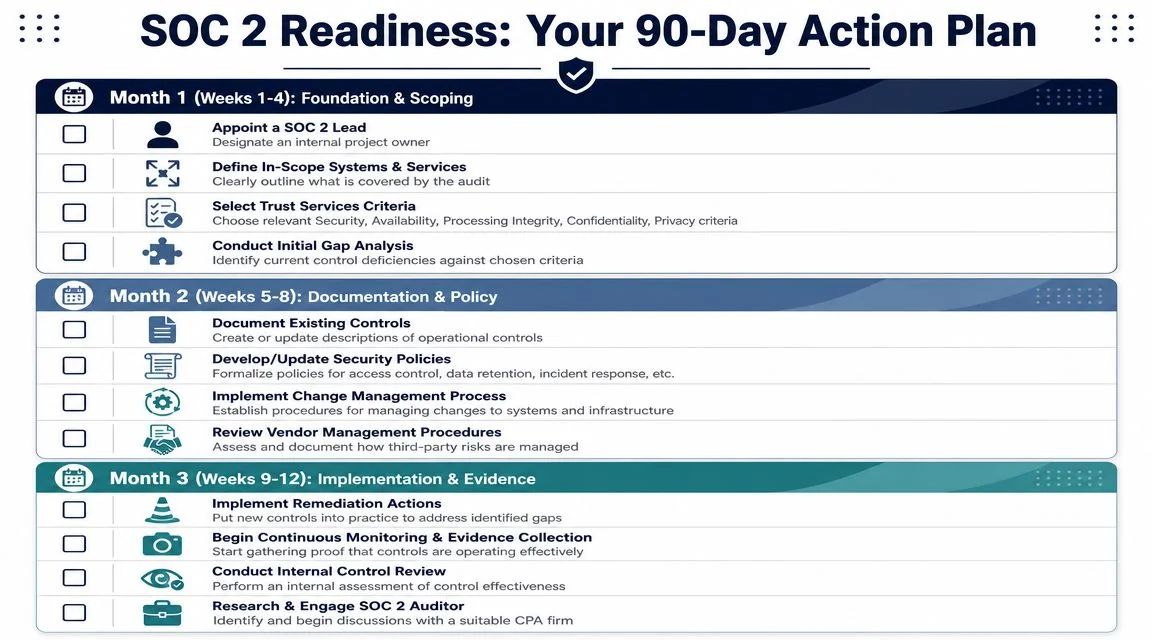

Your First 90 Days of SOC 2 Readiness

A small company doesn’t need a massive compliance function to begin. It needs a disciplined first quarter. The best early moves are boring on purpose: define scope, assign ownership, write down how work is supposed to happen, and start collecting proof that it does.

Days 1 through 30 build the foundation

Appoint one internal lead. Not a committee. One owner.

Then define the business driver. Are you trying to unblock an enterprise deal, satisfy a renewal, prepare for a larger sales motion, or establish a stronger baseline before growth? That answer affects scope, timing, and whether Type 1 is a short-term bridge or just a distraction.

Use the first month to lock down:

- In-scope systems and services

- Selected Trust Services Criteria

- Initial gap analysis

- Named control owners across engineering, IT, HR, and leadership

Days 31 through 60 turn process into documentation

Now document what already exists and identify what doesn’t. Focus on policies and procedures that support access control, change management, incident response, logging, and vendor management.

This is also a good time to review operational edge cases. If you build in a regulated space, practical engineering resources can surface workflow risks your policies need to reflect. For example, Monito’s app testing insights are useful for teams thinking through how testing discipline intersects with reliability, privacy, and production change risk in health-related applications.

Days 61 through 90 start the real operating model

By month three, the work should shift from drafting to operating. Start the recurring reviews. Capture approvals. Save evidence in an organized repository. Begin initial auditor conversations with a short description of scope, environment, and timing goals.

A strong first 90 days usually ends with three things in place:

- A realistic project plan

- Control owners who know their cadence

- An evidence trail that can survive scrutiny

SOC 2 readiness is where a successful soc 2 audit for small business begins. If your team can define scope clearly, assign ownership early, and operate controls consistently before fieldwork starts, the audit becomes a verification exercise instead of an emergency cleanup project. That’s what shortens delays, protects senior time, and gives you the best chance of earning a report that helps sales, builds trust, and scales with the business.